Two Billion Light Up: The South Asian Electric Wave

…In the electric age, platinum,

…But when Orion and Sirius are come into mid-heaven, and rosy-fingered dawn sees Arcturus, then cut off all the grape-clusters, Perses, and bring them home

Hesiod, Works and Days

Ancient peoples looked to the heavens for guidance, knowing that the appearance of certain constellations in the night sky forewarned of an impending change of season. In like manner, the shift from an age of plenitude to one of soaring prices and scarcity has been often foreshadowed by manifestations of certain portentous phenomena.

At time of writing, the signs indicate that such irresistible and invisible forces are bubbling away in the background, an empyreal brew that is likely push commodity prices into an upward trajectory over the decade ahead.

Mainstream commodity cycle forecasts tend to be grounded in conjecture about the impact of monetary-policy settings on the behaviours of populations, or on second-guessing the policy initiatives of governments worldwide. Here, the focus is on forces more sublime.

Our modus operandi lies in the past. As will be illustrated in these pages, all major commodity booms within recent history have been presaged by a number of signature characteristics, offering important cues that can betray the emergence of a new great up-cycle before it roars into life.

Currently, such signals indicate that the shadow of a new great boom is looming closer.

A powerful bicephaly of macro forces have begun to materialise, and over the past two centuries the appearance this double Draconis has been a reliable harbinger for the emergence of a new age of high commodity prices.

Confronted for the first time by the bewildering vastness of the stock-index of a major securities exchange, the tyro investor will soon apprehend the division of the stocks into two disparate camps, known as the Industrial and the Material sectors.

An idiosyncrasy of the stock-markets of the mining driven economies of Australia and Canada are the sheer number of stocks that comprise the Materials sector of these exchanges, a category also commonly called the Resources sector. The majority of the stocks that constitute this sector are small exploration companies seeking out valuable minerals.

This class of stock blooms during booms, with the share prices of most of the resource stocks riding the rising trajectory of commodity prices. However, when commodity prices are lacklustre- and this has generally been more often the case than not in recent history – the capital intensive resource stocks, and their share prices, struggle to stay afloat.

The converse is true for industrial stocks, to a lesser extent. When commodities are expensive, high energy prices and skill shortages present a challenge to most stocks outside the mining sector, and many such stocks invariably lag as a result.

Committing to either of these sectors represents a call on the future direction of commodity prices, even if individual investors may not always be cognisant of this.

An investor who decides to back a conservative stock such as Microsoft, for example, inadvertently signals an expectation that commodity prices will remain subdued over the foreseeable future.

Extended commodity booms are characterised by high energy prices and elevated interest rates, resulting in tangible assets becoming expensive to replicate and thus more valuable over such periods. Microsoft is a company with few tangible assets relative to its market valuation and will thus likely prove a laggard in the event of a new commodity boom.

This invariably leads to the question as to whether an individual investor has any hope of reliably anticipating the long term path of commodity prices.

As argued above, the most reliable way of foretelling future movements of commodity prices lies in looking to the past, recognising the factors that presaged the major commodity booms within recent history.

Major commodity booms are anomalous events, the product of a peculiar set of conditions, and it is notable that each of the major booms of the past has been preceded by a number of signature characteristics.

A forewarned observer should theoretically be able to identify these characteristics as they come to pass. When a number of these coalesce, it can be taken as a strong indication that conditions are ripe for formation of a new commodity up-cycle.

One caveat to bear in mind in relation to this stated objective is that the focus here is on long-term movements in commodity cycles (the so-called ‘super-cycles’), rather than the less predictable short term price fluctuations.

In this essay, the focus will be on the three most recent long-term upcycles in commodity prices, all of which occurred within the past two centuries. The particular emphasis will be on two notable macro themes that conjunctly may have flagged the emergence of these great booms.

Short-term surges in commodity prices are a relatively common occurrence, driven by supply disruptions or a sudden spike in demand which overwhelms the readily available supply.

In rare instances, as during the First World War, the extent of the supply-demand mismatch is of such a magnitude that elevated prices are sustained over multiple consecutive years. However, the more usual experience is for such price resurgences peter out within a year or two.

Higher prices provide a strong incentive for commodity producers to ramp-up production, and likewise, end-users of commodities have an incentive to reduce their consumption of materials when prices are elevated, the high prices prompting them to adopt thrifty, money-saving practices.

Occasionally, however, the supply-demand equilibrium goes off-kilter, and commodity prices enter long-term upcycles lasting for years, sometimes even decades. Three of these rare, long upcycles in commodity prices will be detailed here.

The first such great boom, commonly dubbed the ‘Gold Rush’ era, commenced in the aftermath of the Revolutionary and Napoleonic Wars of the early 19th Century, leading to a sustained, long-term rise in commodity prices. The prices of most commodities attained their apogee only in the early 1860s, as the American Civil War raged.

A painful and extended bust followed this remarkable boom, and commodity prices eventually bottomed out in the 1930s, during the aptly named Great Depression.

A second great boom would emerge shortly afterwards, in the wake of the devastation of the Second World War. Although commodity prices had eased by the late 1950s, at the end of the 60s they were enjoying a steady resurgence, and the price of many commodities- oil, gold, and silver, to name a few- entered a final, phenomenal boom phase before the 1970s had ended.

The last and most recent great commodity price surge commenced in the early years of this century and is widely associated with the rise of China as a major economic power. The ‘China boom’ lasted just under a decade, with commodity prices wanning over the 2010s.

It would be onerous to record the numerous individual factors that may have contributed these booms, so instead the focus here will be on two macro forces that together seem to have acted as particularly influential drivers.

The first of these great forces is a demographic slough, or trough, in the years leading up to the boom years. The second is disease: pandemics, or major epidemics, that impact multiple regions of the world.

Whenever these twin forces have crossed paths within the past two centuries, the result has been multi-year surges in the price of commodities.

The first commonality of these three booms is that all were preceded by a ‘demographic trough’. An extended baby-drought, a stretch of years of abnormally low birth-rates, took place some thirty years before each of these great booms.

Historically, lengthy periods of warfare have been a common cause of this phenomenon.

During extended wars, the mass dispersal of personnel to theatres of war abroad results in large number of able-bodied men leaving their hometowns and villages for an extended period. The predictable consequence of this is sub-par birth rates over the course of the conflict, and often for years afterwards.

It is notable that the first of the two great commodity booms of the modern era, the restless years of the ‘Gold Rush’ era and the major boom that emerged in the aftermath of World War II, both emerged some three decades after major periods of warfare.

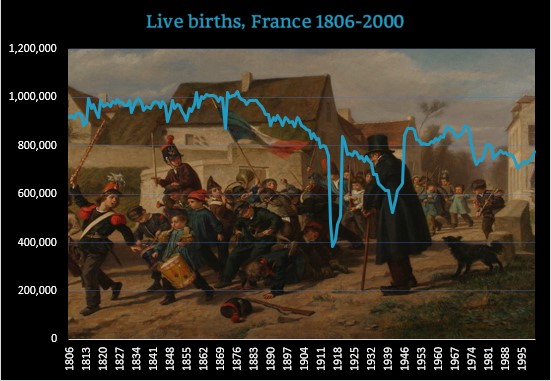

The earliest concrete surviving records detailing the impact of war on birth-rates date back to France in the early 19th century, during the tumult of the Napoleonic Wars. Although the birth-rate figures for France meander without any significant pattern in the first decade of that century, there was a substantial fall in the number of births recorded over the years 1811-12, coinciding with Napoleon’s invasion of Russia. (1)

France would not have been the only nation to experience a dip in birth rates in this period. The last years of the Eighteenth Century and the early years of the Nineteenth Century were characterised by epic conflicts across Europe and abroad. In Europe, the Napoleonic wars led to widespread devastation, while across the Atlantic, Revolutionary wars would set the Americas on fire.

Such major conflicts invariably adversely impacted the number of births in these regions, and this appears to have been the first tumbling domino to set into train the great commodity boom of the Gold Rush era, the first of the three great commodity booms of the modern era.

For a similar reason, a century on, birth rates plunged during the two World Wars, with most of the belligerent nations of these destructive conflicts experiencing a baby-bust during these years of turmoil. While the 1920s saw a modest recovery in the birth rates of many countries, the subsequent ‘Great Depression’ in the 1930s impacted both economic growth and birth-rates around the world.

In summary, the thirty year period from 1915 to 1945 was characterised by flat birth-rates, and as in the early 19th Century, an extended period of high commodity prices followed some thirty years after this baby-bust, with commodity prices heading in a steady upward trend from 1945 to around 1980.

Lastly, a significant dip in the birth-rate is also apparent in the 1970s, both in the Western World and in China, although in this instance it resulted from an altogether different cause.

In the Western world, the combination of a sharp increase in the rate of female workforce participation and wider access to family planning measures resulted in low birth rates over the 1970s, whereas in China over the same decade the government introduced measures to restrict the size of Chinese families, culminating in the one-child policy of 1979. (2)

As the world entered a new millennium some thirty years after the baby-bust of the 70s, a new commodity super cycle roared to life, for the third time in two centuries.

A key question arises out of this, namely, why it is that great commodity booms seem to emerge some three decades after periods of low birth-rates?.

While the answer this question is open to speculation, it should be noted that the thirty year-old demographic cohort more-or-less represents the emerging skilled and able-bodied workforce in a population.

A dip in the birth-rate will thus invariably result in a shortage of skilled workers thirty years hence, and if this shortfall is sustained, a skills-shortage will ensue, leading to higher wages which then flows through to commodity prices.

It is also worth bearing in mind that mining operations are capital intensive and hazardous affairs, and if younger investors, who would tend to be less risk averse, are in short supply, that would make it more difficult for hopeful miners to raise capital.

The tendency of commodity booms to emerge around three decades after a demographic trough may thus be a consequence of a shortfall of both skilled workers and of risk-tolerant investors willing to fund mining ventures.

While the lingering, long-term impact of major wars seems to have some role in sowing the seeds for future commodity booms, War is not the only of the ‘Horsemen of the Apocalypse’ with a part to play in ushering in new commodity booms.

Pestilence, terrible outbreaks of disease, is a second agent frequently associated with the stirrings of great commodity booms.

The three great commodity booms of modern times -that of the Gold Rush era, the commodity surge of the 1970s and the China boom of the early 2000s- were each preceded by exceptionally virulent outbreaks of disease.

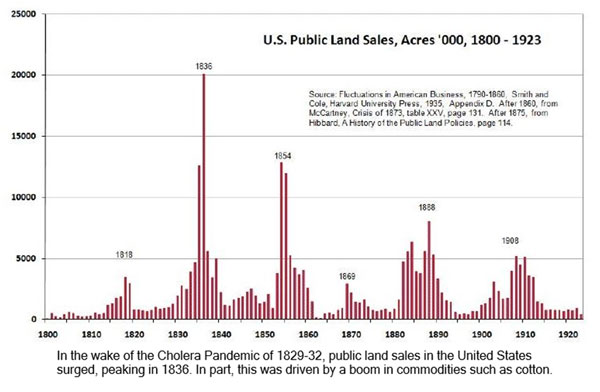

The Cholera Pandemic: The first of these commodity super-cycles, the ‘Gold Rush’ boom of the 19th century, marched almost hand-in-hand with a major new epidemic, cholera, which commenced its advance across the globe between 1829 and the 1830s. Periodic outbreaks of the same disease reoccurred over the remainder of this era.

Hong Kong Flu: In a similar vein, the extraordinary commodity price surge of the early 1970s was preceded by the devastating ‘Hong Kong’ flu pandemic of 1968-1970.

After first being identified in Hong Kong in July 1968, this highly contagious virus had spread to almost every continent by early 1969. The United Kingdom recorded over 30,000 deaths linked to this strain of influenza in that year, while the death toll in the United States climbed as high as 100,000.

For Australia and Japan, a second wave of the viral influenza between 1969 and 1970 proved more deadly than the first wave, evident from the conspicuous spikes recorded in the mortality figures for these nations in that same year.

Across the globe, the total death toll from the successive waves of the pandemic was estimated to be at least one million. (4)

SARS: Lastly, the ‘China Boom’ of the early 2000s also kicked off in the wake of an epidemic, in this instance the SARS outbreak. Starting from November of 2002 and into the new year, China experienced a flareup of the Severe Acute Respiratory Syndrome virus, infecting several thousand people in China and abroad.

The World Health Organisation declared the disease contained in July of 2003, and before the year was over, most commodity prices had begun to roar to life, marking the start of the ‘China Boom’ that was to characterise the first decade of the 21st century.

The frequent overlap between major epidemics or pandemics and the onset of great commodity booms once again solicits the question as to whether these disparate developments spring from some common catalyst.

In this instance, technology might be the common thread. It is notable that epidemics of disease have tended to correlate with dramatic advances in transportation technologies.

The major cholera epidemics of the 19th century coincided with the emergence of steam-ships and steam-trains, just as the Hong Kong Flu pandemic of the late 60s followed on from the introduction of affordable jet passenger services.

These technologies invariably serve to disperse infectious diseases to all corners of the globe, but the flipside of such technologies is that they also promote mobility, thus increasing the pool of opportunities for skilled workers.

This has a powerful wealth-creation effect, leading to more skilled workers venturing abroad to seek their fortune, which soon feeds into skill shortages, lower unemployment and to higher wages in the old country. As greater prosperity takes hold, goods and services once seen as luxuries become necessities, resulting in increased consumption.

With the ranks of the middle class swelling, increased spending and consumption follows, feeding into greater demand for scarce commodities, and in time this promotes new mining booms.

Over the course of modern history, the double-act of the Demographic Trough and its sometimes collaborator, the Viral Pandemic, have thrice over proven to be symptomatic of an impending bout of elevated commodity prices.

Weighed against this, one important caveat must be noted, namely unemployment. Not one of the three great commodity booms illustrated above emerged from periods of mass unemployment.

This would seem to make sense. Given enough time, a surplus of labour invariably translates to a surplus in the supply of commodities.

Any tangible commodity is the product of the toil of human labour, and with excessive unemployment rates tending to have a depressive effect on wages, high unemployment would help to grease the wheels of commodity production, thereby boosting supply and capping commodity prices.

Steep unemployment rates may also lead to reduced consumption, even on the part of those who are still employed. The uncertainty of periods of elevated employment may prompt frugal behaviour on the part of consumers, still further crimping demand for consumables and the commodities from which they are made.

High unemployment levels thus appear to be a stumbling-block for sustained commodity booms, and based on the antecedents of modern history, a sustained fall in unemployment is an important milestone for the commencement of an extended boom-phase.

The Bicephalic Dragon is a powerful but extremely rare two-headed monster, occurring in the mythology of a number of cultures.

This two-headed dragon is an apt metaphor for the twin trends that have been the object of our focus here. The ‘Demographic Trough’ represents one of the heads of the beast, and ‘Viral Epidemics’ represents the other.

By themselves, each of these macro trends represent a formidable, earth-shaking force. Together, they may be nearly irrepressible.

Today, this two headed monster is casting its shadow over the world.

The first head of this monster is the Demographic Trough. Fertility rates and have been falling in every region of the world for decades. Since the 1990s, this decline has been particularly acute in the nations that comprised the former Soviet Union, as well as in China. Most of these countries, it should be noted, are major commodity producers.

In consequence, the working age population in many nations in the world will steadily decline over the decade ahead. As has been highlighted above, when a new generation of thirty-somethings is smaller than the one that preceded it, long commodity booms have tended to follow in their wake.

While the emergence of a demographic trough in the working-age populations of commodity producing nations is an indicator that a commodity boom is looming, it is the hand of Pestilence that often seems to fire the starting pistol.

Epidemics of disease frequently serve as signals that conditions are ripe for a sustained commodity boom. In the modern era, major epidemics or pandemics have taken place on the eve of three major booms: during the cholera pandemics of the 1830s; again, in the years of the Hong Kong flu pandemic at the tail end of the 1960s, and in 2002-03 during the SARS outbreak.

Today, in a world haunted by imperceptible pathogens, investors might be inclined to rush into apparent safety of conservative blue-chip stocks. Yet this instinctive reaction may be wrong.

As has been outlined in the paragraphs above, the confluence of a Demographic Trough in the working age population with a major outbreak of disease have occurred on only three occasions within the past two centuries: During the 1830s; the years between 1968-1970, and again in 2002-2003.

In all three instances, major commodity booms, lasting many years, followed in the wake of the emergence of this two-headed dragon.

This is not to say, however, that such a scenario is certain to pan out in the short-term.

One major bar that needs to be first vaulted is that of elevated unemployment. The two great booms of the past century were hatched in periods of modest-to-low unemployment in the major mining nations of the world.

Modest to low unemployment thus appears to be a precondition for the emergence of a new season of commodity scarcity.

********

The focus of this essay has been on the influence of two forces of nature, disease and demographics, as powerful drivers of commodity prices.

This should not be taken to infer that the fruits of human artifice do not bear any influence on the path of commodities.

One industrial technology has a time-tested capacity to charge the prices of certain commodities, and the evidence over recent years suggests that it is set to do so once again.

Our lens shall be next trained on a everyday but often underestimated technology whose paroxysmal and uneven march from continent to continent has almost always packed a transformative punch.

Footnotes

(1) Louis I Dublin, War and the Birth Rate- A Brief Historical Summary, American Journal of Public Health, 1945 p 315

(2) Martin King Whyte, Wang Feng and Yong Cai, Challenging Myths About China’s One Child Policy, The China Journal, 2015, p 149

(3) Data complied by Phillip Anderson.

(4) Mark Honigsbaum, Revisiting the 1957 and 1968 influenza pandemics, The Lancet, 2020 (view link)

Patrick Frayne is a Sydney-based mining historian and writer with a long-standing interest in commodities cycles and their influence over history. His research articles have been published on a number of Financial Media and History websites.

…In the electric age, platinum,

What does it take for

The skies are brass and the plains

…Gold and silver have, uninterruptedly to

…In the electric age, platinum, and quartz, and every existing substance can be melted and distilled or sublimed. Thus, mighty new industries